- LittleLaw

- Posts

- 🔐 This law could make the UK a crypto hub

🔐 This law could make the UK a crypto hub

Idin Sabahipour & Laura White

September 18, 2024

In partnership with

Table of Contents

If you take just one thing from this email…

The Property (Digital Assets etc) Bill aims to give digital assets, like cryptocurrencies, the same legal protection as physical property. This would mean that owners of digital assets can seek justice for theft or fraud. The added protection to these assets could mean the UK becomes a more prominent crypto hub. Also, law firms with expertise in digital assets may see more opportunities in those matters.

EDITOR’S RAMBLE 🗣

Last week I shared a poll to see if people were down for a LittleLaw meet-up.

The response has been insaaaane (more than 300 people said yes). So, we’ve already been busy to try to make it happen.

I can’t share much more yet, but keep your eyes on next week’s newsletter.

- Idin

FEATURED REPORT 📰

🔐 This law could make the UK a crypto hub

Credit: Giphy

What's going on here?

Should the law treat digital assets (like Bitcoin) the same way it treats your physical property (like your laptop)?

The Property (Digital Assets etc) Bill was introduced to Parliament this week — and it suggests that personal property rights should be extended to digital assets. The Bill is based on this report by the Law Commission (an independent body which reviews the law in England & Wales).

Why do we need this Bill?

Under the laws of England & Wales, personal property rights apply to two types of ‘thing’ (which are called ‘choses’ – based on the French for ‘thing’):

Choses in possession: Tangible, physical items you can own and hold (like jewellery, a painting, or a car).

Choses in action: Intangible rights that you can't physically hold but have the legal right to enforce. For example, if someone owes you money (a debt), you have the right to take legal action to collect it. So, the right to claim or enforce something through the courts (like a debt or contract right) is a chose in action.

If you own cryptocurrency (or other digital assets like NFTs), they aren't a chose in possession because they’re intangible. They’re also not a chose in action because you can’t recover them through legal action (they exist through a distributed ledger, outside of the legal system).

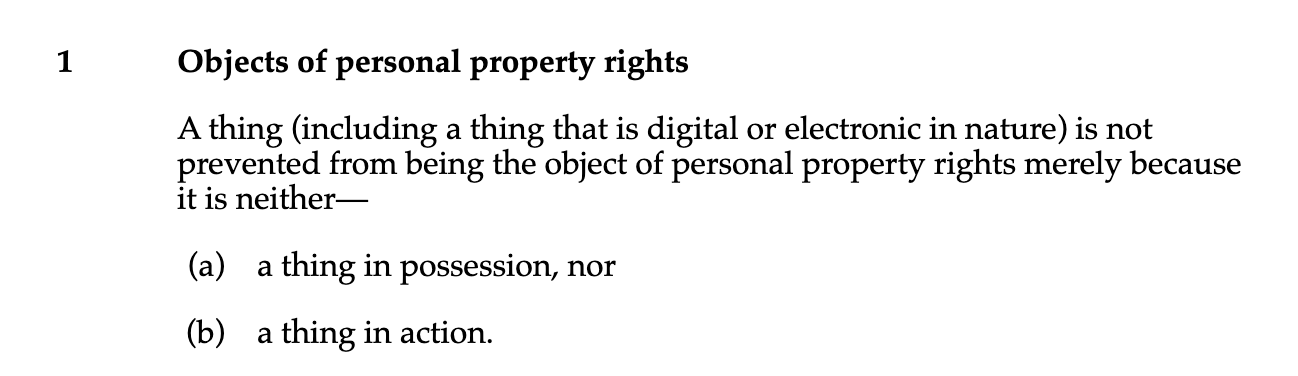

So, clause 1 of the Bill (which you can read in full here) proposes a new, third category of personal property.

This (in a roundabout way) includes cryptocurrencies and similar digital assets, giving them personal property rights.

What will fall into this third category?

In its report, the Law Commission didn’t define explicitly what digital assets fall within this third category. It believes that common law (cases decided by the courts) is better placed to determine this.

But, the Commission gave a list of characteristics which, if present, mean a digital asset should benefit from personal property rights:

It includes electronic data, like computer code or digital signals,

It exists on its own, separate from people or the legal system, and

It is “rivalrous”, meaning only one person can use it at a time, so if one person uses it, others can’t.

So, cryptocurrencies (like Bitcoin and Ethereum), would satisfy all of these characteristics.

Why should law firms care?

Clearer legal rights: Right now, digital assets don't have the same legal protection as physical property. This means owners aren’t sure what they can do if their assets are hacked or stolen. The Bill will give digital assets the same rights as physical property, like jewellery. This means that people can seek justice for theft or fraud of their digital assets. This opens up opportunities for law firms to represent clients in these cases.

Easier distribution of digital assets: The lack of property rights for digital assets creates issues in situations like bankruptcy or divorce, where assets need to be divided. The Bill would mean digital assets are treated like any other property — so, for example, they can be used to repay creditors if a company becomes insolvent. Law firms would need to consider this change when representing clients with digital assets who are in these situations.

UK’s prominence in crypto: By establishing clearer legal protections, the Bill also strengthens the UK’s position as a hub for digital asset businesses — this would encourage more companies to operate and invest here. As the digital assets sector currently contributes £34 billion a year to the UK economy, its growth could mean new business for commercial law firms, particularly in advising companies on compliance, transactions, and disputes involving digital assets like crypto.

Fintech law firms specialising in blockchain and cryptocurrencies

(Chambers and Partners)

What are other countries doing?

The US, EU, Japan, and Brazil are working on (or have already put in place) rules for digital assets. For example, the EU has introduced broad crypto regulations, and Brazil’s central bank oversees crypto assets there.

But, if the Bill passes, the UK will be one of the first countries to legally confirm that personal property rights apply to digital assets, positioning it as a leader in the global digital assets market. 💪

When does the Bill come into force?

The Bill is currently at the first stage of the process – it’s only just been introduced in Parliament.

Before it becomes law, here’s what needs to happen:

Second reading: A general debate in Parliament about the Bill’s main points.

Committee stage: A detailed review of the Bill, where amendments can be proposed.

Report stage: Another chance to suggest and discuss changes.

Third reading: The final opportunity for Parliament to debate and make adjustments.

The other house: The Bill goes through similar steps in the House of Lords.

Royal Assent: If both Parliament and the House of Lords approve, the Bill will receive Royal Assent and officially become law (it’ll go from a ‘Bill’ to an ‘Act’).

This process can take months (or longer), depending on agreement in Parliament and the House of Lords. The Bill could be changed, or even fail if it doesn’t get enough support. Also, even if it becomes law, different parts may take effect at different times — so it’ll be one to watch.

TOGETHER WITH 1440* 🤝

Receive Honest News Today

Join over 4 million Americans who start their day with 1440 – your daily digest for unbiased, fact-centric news. From politics to sports, we cover it all by analyzing over 100 sources. Our concise, 5-minute read lands in your inbox each morning at no cost. Experience news without the noise; let 1440 help you make up your own mind. Sign up now and invite your friends and family to be part of the informed.

* This is sponsored content

IN OTHER NEWS 🗞

🎓 Freshfields has set a new social mobility target for its UK trainee intake. From the 2024-2026 recruitment cycle, they aim for 20% of their trainees to come from lower socioeconomic backgrounds. They’re using a common measure for this—looking at what the trainee's parents did for work when the trainee was 14. Freshfields says it will review the target after 2026 to see how it's going and make changes if needed.

📚️ WH Smith announced a £50 million share buyback after an increase in travel resulted in more sales. Its UK travel stores in airports and train stations were up 10% in sale thanks to more passengers. This boost in cash flow led to the buyback (companies do share buybacks to reduce the number of shares in the market, which can drive up the share price and return value to shareholders). In fact, just the news of the buyback already lifted its value by 12%. You can read more about share buybacks in this article we wrote.

🏢 Hogan Lovells is closing its offices in Warsaw, Sydney, and Johannesburg. The move has come as the firm wants to focus on key markets like London, New York, and California. CEO Miguel Zaldivar said it was a tough decision but necessary for the firm's growth. This news comes shortly after A&O Shearman announced it would also be closing its Johannesburg office.

⚖️ Tesco lost a big case in the Supreme Court brought by the shop workers' union, Usdaw. Back in 2007, some employees got a 'permanent' pay supplement for relocating to a new site. But in 2021, Tesco threatened to fire and rehire them on worse terms if they didn't give up the extra pay. The Supreme Court ruled that Tesco (represented by Freshfields) couldn’t do this, as their contracts implied the supplement was part of their employment rights.

🇪🇺 The EU competition team had two major wins this week. The European Court of Justice ruled against Apple’s tax deal with Ireland, demanding $14.4 billion in back taxes. It also upheld a $2.6 billion penalty against Google for competition violations. These cases highlight growing pressure on Big Tech from regulators in both Europe and the U.S.

AROUND THE WEB 🌐

🍽️ Fun: Find attractions and restaurants in any city, sorted by number of reviews

😺 Odd: Want to bounce some cats? (yup, that’s it)

📖 Read: This site picks you a book to read based on your mood

Credit: r/internetisbeautiful

STUFF THAT MIGHT HELP YOU 👌

📹️ Free application help: If you're applying to commercial law firms, check out my YouTube channel for actionable tips and an insight into the lifestyle of a commercial lawyer in London.

How did you find today's newsletter? |