- LittleLaw

- Posts

- ⚡ Inside a private equity deal investing in data centres

⚡ Inside a private equity deal investing in data centres

Idin Sabahipour

March 25, 2026

Together with

Table of Contents

If you take just one thing from this email...

In private equity, lawyers don’t decide whether a deal is a good investment – they’re the ones that make sure the deal can actually happen.

That means structuring the acquisition, spotting risks in due diligence, protecting the buyer in the documents, and dealing with contract or regulatory issues that could delay or damage the deal.

EDITOR’S RAMBLE 🗣

I think the most talked-about area of work among aspiring lawyers is “private equity” (we get more opens when PE is mentioned in the email subject, like today 👀).

But I've noticed something. A lot of people say they “want to work in PE” – but far fewer can actually explain what lawyers do on a PE deal, beyond something like "they help buy companies, improve them, and sell them” (spoiler: the lawyers don’t do any of that).

That knowledge gap is exactly what this week's newsletter is trying to close.

We partnered with Fried Frank to go behind the scenes of a real private equity transaction – TowerBrook Capital's acquisition of a stake in JSM (a business that builds data centre infrastructure).

It was a super interesting deal to break down. And if private equity is an area you want to work in (or even just talk about convincingly in applications) you'll like this one.

Once you've read it, please could you complete this 2-second poll further down? I'd love to hear your thoughts on this newsletter.

– Idin

P.S. Fried Frank’s TC application window is open now. To apply, click here.

FEATURED REPORT 📰

⚡ Inside a private equity deal investing in data centres

What’s going on here?

TowerBrook Capital Partners (a private equity firm based in London and New York) acquired a majority stake in JSM Group Services.

JSM builds and maintains the systems that keep data centres, and other large sites, running.

🤔 What is a data centre?

A data centre is a large, secure building filled with computer servers.

Those servers store data and run online services like cloud storage, streaming platforms, and AI tools.

To work properly, data centres need constant power and specialist electrical infrastructure (that’s the kind of thing JSM provides).

As cloud computing and AI grow, more data centres are being built. By investing in JSM, TowerBrook backed the infrastructure that supports data centres, rather than the data centres themselves.

Fried Frank advised TowerBrook on the deal. They helped structure and complete the acquisition.

When do lawyers like Fried Frank get involved?

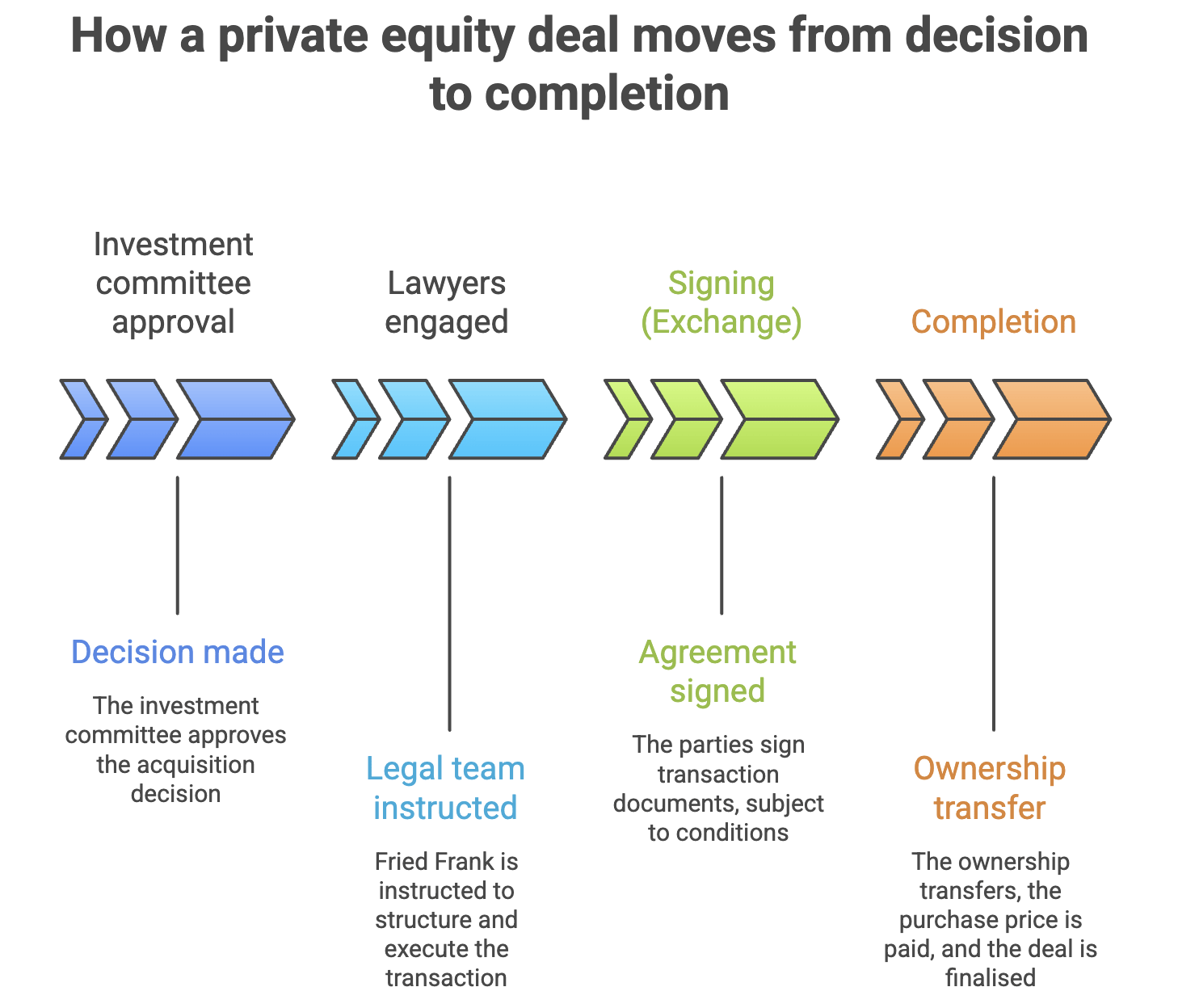

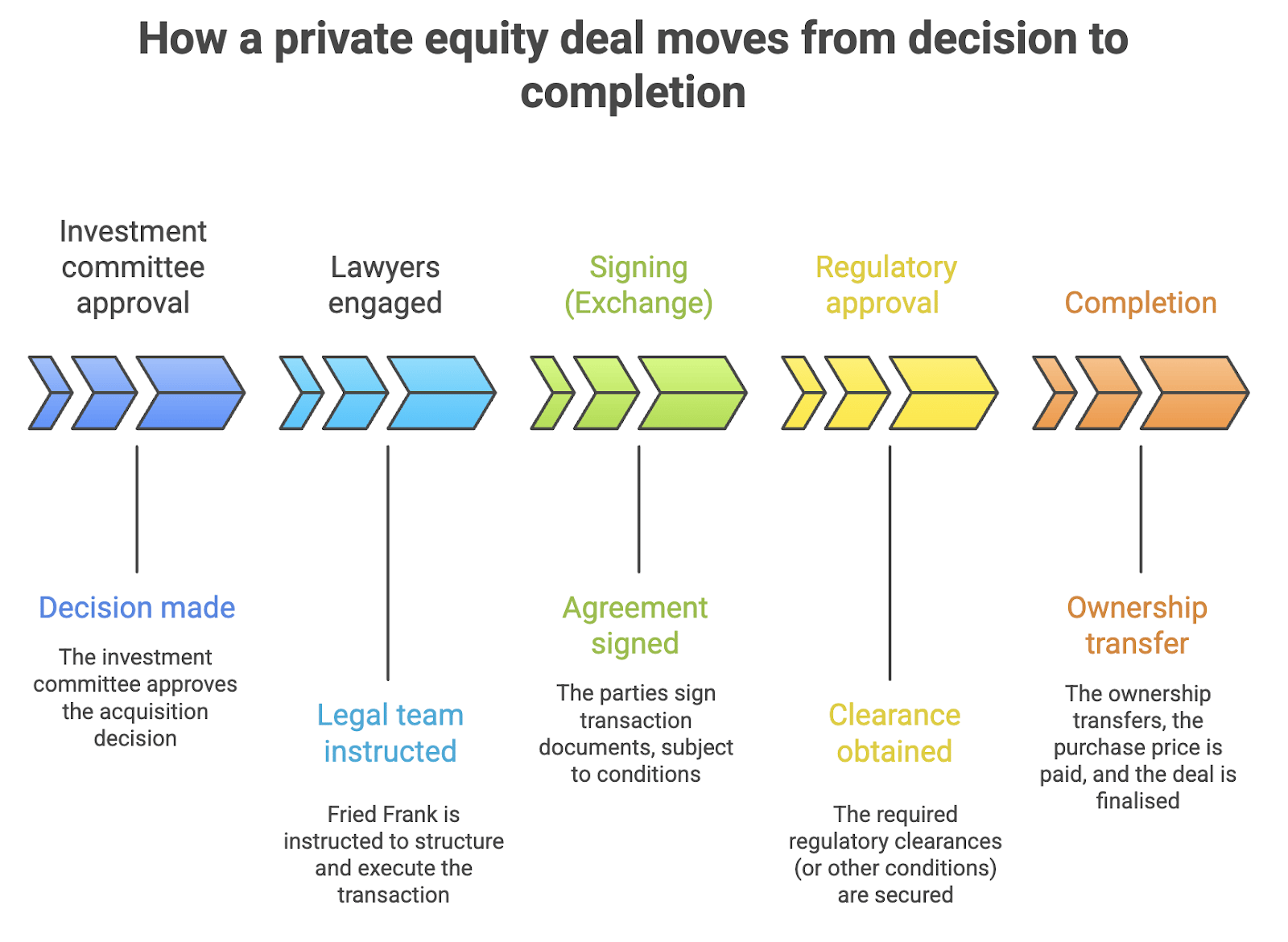

On deals like this, lawyers are usually brought in after the private equity firm’s investment committee has initially approved a deal.

🤔 What is an investment committee?

In a private equity firm, the investment committee is the group that makes the final decision on whether or not to invest, based on the target company’s business model, risk profile, and strategy.

Once the PE firm approves a deal, the focus shifts from whether to invest to how to complete the transaction – and that’s when Fried Frank gets more involved. Their work is time-sensitive, with deals often running on a tight timetable (this deal had around one month to complete).

The lawyers’ job is to turn the investment decision into a completed transaction.

What legal work did Fried Frank handle on this deal?

The work Fried Frank did can be broken down into a few key areas.

🏗️ Structuring the acquisition

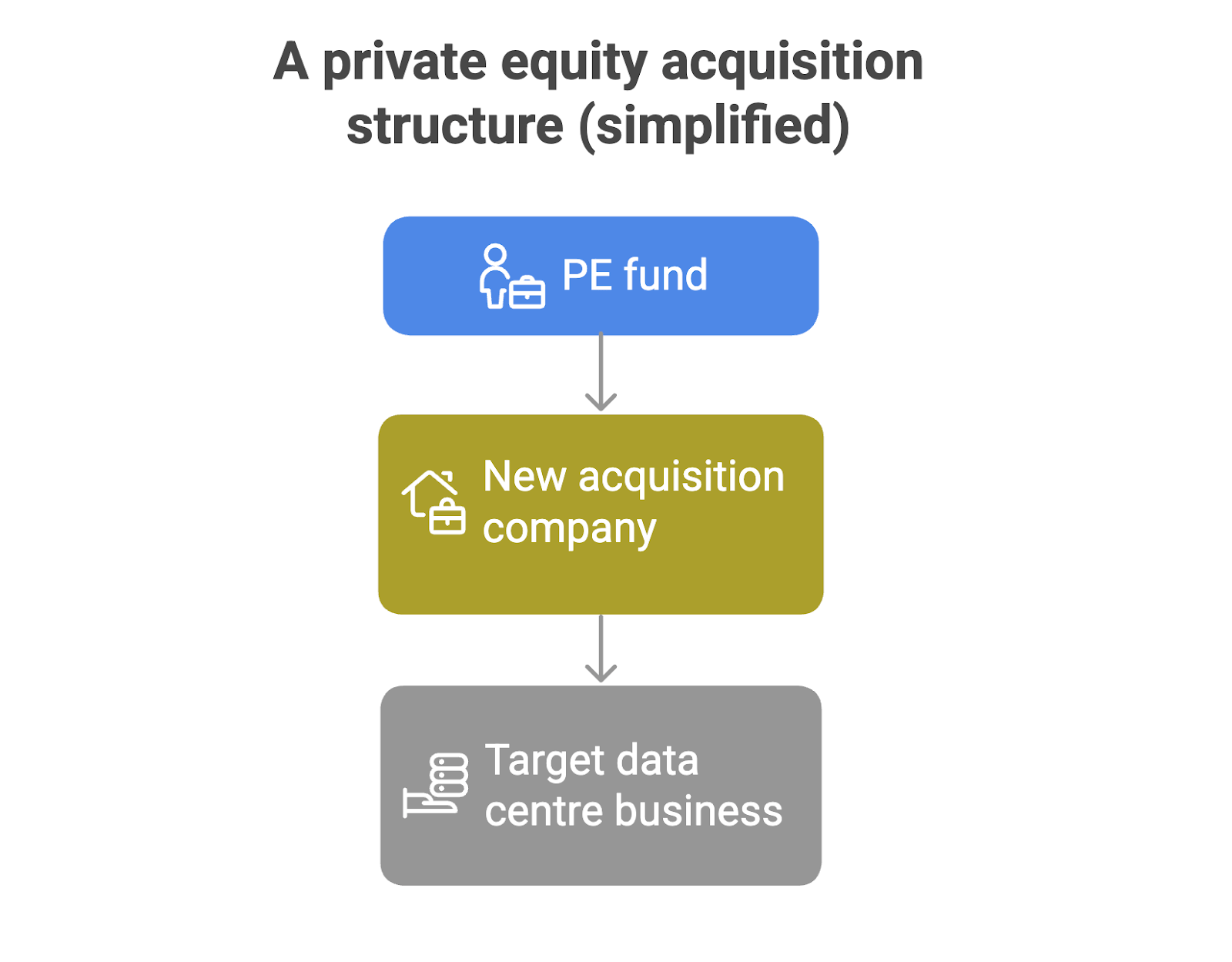

One of Fried Frank’s first tasks (alongside the tax advisors) was creating the legal structure for the acquisition.

In private equity deals, the buyer doesn’t usually purchase the target company directly. Instead, lawyers set up one or more new companies to acquire and hold the business – they sit between the PE fund and the target business.

The reason for this is that it allows the private equity firm to:

Separate risk: If something goes wrong, the problem stays with that business (not the rest of the fund)

Clarify control: It’s clear who owns the company and who has decision-making rights

Raise debt at the right level: Borrowing sits with the acquisition company (not the fund)

Plan for an eventual exit: Eventually, the PE firm can sell the acquisition company

Getting this structure right at the start is important. Once the deal completes, it can be difficult to change it.

🔍 Due diligence

Before seeking approval from its investment committee, TowerBrook carried out legal due diligence on JSM’s business.

🤔 What is due diligence?

Due diligence (or “DD”) is the process of checking a business before buying it.

Lawyers carry out legal due diligence to identify risks so the buyer makes an informed decision before signing the deal.

As well as this, investors will often carry out financial, tax and commercial due diligence on the business. Any significant risks that are identified may be addressed either by way of a price reduction or through legal protection in the transaction documents (such as warranties or indemnities).

The aim of due diligence isn’t to remove all risk (some risk is unavoidable). The goal is to identify the most important issues and understand how serious they are.

Where there is a risk, TowerBrook can get legal advice to mitigate it. In some cases, the buyer may accept the risk. In others, it can lead to changes in the deal terms or added protections in the transaction documents.

📝 Drafting the transaction documents

Fried Frank was responsible for drafting and negotiating the main transaction documents.

The main document in a deal like this is the share purchase agreement (or “SPA”). This sets out the core terms of the transaction, including the price, when the deal can complete, and any conditions that must be met first.

The SPA also includes warranties. You can think of warranties as a set of promises from the seller about the business. For example, the seller may promise that key contracts are in place or that the company is complying with the law. If one of those promises later turns out to be wrong, the buyer may have a right to claim against the seller.

There’s also a second key document called a shareholders’ agreement. This document, along with the articles of association, sets the rules between all the shareholders in the company. In this case, it would state how TowerBrook (as majority shareholder) works with any founders, managers and co-investors who stay invested as minority shareholders after the deal completes.

Together, these transaction documents are important. They determine who controls the business, how risk is shared, and what happens if things don’t go as planned after completion.

🔐 Signing and completion

Signing and completion in a corporate transaction are not the same thing:

Signing: When the parties formally agree to the deal by signing the transaction documents (ownership doesn’t change yet)

Completion: The moment the deal actually takes effect (money is paid, and ownership changes hands)

Between signing and completion, certain steps (or “conditions”) usually need to happen. These can include things like regulatory approvals – which we’ll come back to later.

On completion, Fried Frank coordinated the final steps of the process – making sure funds moved to the right parties, fees were paid, and any existing debt was dealt with as planned.

While you’re reading this, could you imagine yourself working at Fried Frank?

Why did this deal need specialist legal advice?

Data centre infrastructure deals like this raise some legal issues that don’t come up in a standard business sale.

On this transaction, there were two important areas: customer contracts and regulation.

1. The importance of customer contracts

During due diligence, any key contracts were reviewed to understand their length, pricing terms, and termination rights.

One important question that often comes up on share acquisitions is what would happen to these contracts if the business changed owner. Sometimes customer contracts can include a change-of-control clause.

🤔 What is a change-of-control clause?

A change-of-control clause is a rule in a contract that applies if a business is sold or gets a new owner.

Imagine you sign a contract to join a gym. If the gym owner sells the business to someone else, you might want the right to cancel (because the service might not be the same under new ownership).

In business contracts, a change-of-control clause gives the other party similar rights. They may be able to approve the new owner, ask for changes to the contract, or end it altogether.

As part of the due diligence process, lawyers advising the buyer need to check whether any contracts include these clauses. If a clause like this is included, lawyers might recommend getting the customer's approval for the sale beforehand, or making sure the potential risks are covered in the deal terms (for example through a price adjustment).

2. How regulation impacted the deal timetable

Data centre infrastructure businesses, like JSM, are heavily regulated because of how critical they are to the provision of digital services across the country.

So, acquisitions in this sector (like this one) can raise foreign investment and national security issues.

On deals like this, lawyers need to consider whether the transaction could trigger review under the UK’s National Security and Investment (NSI) regime.

🤔 What is the NSI regime?

It’s a UK system that allows the government to review and, in rare cases, block or delay deals that could pose national security risks.

Reviews take time, which can affect deal timetables.

When a deal needs to be notified to the UK government, Fried Frank helps manage this process and factor any regulatory review into the deal timetable.

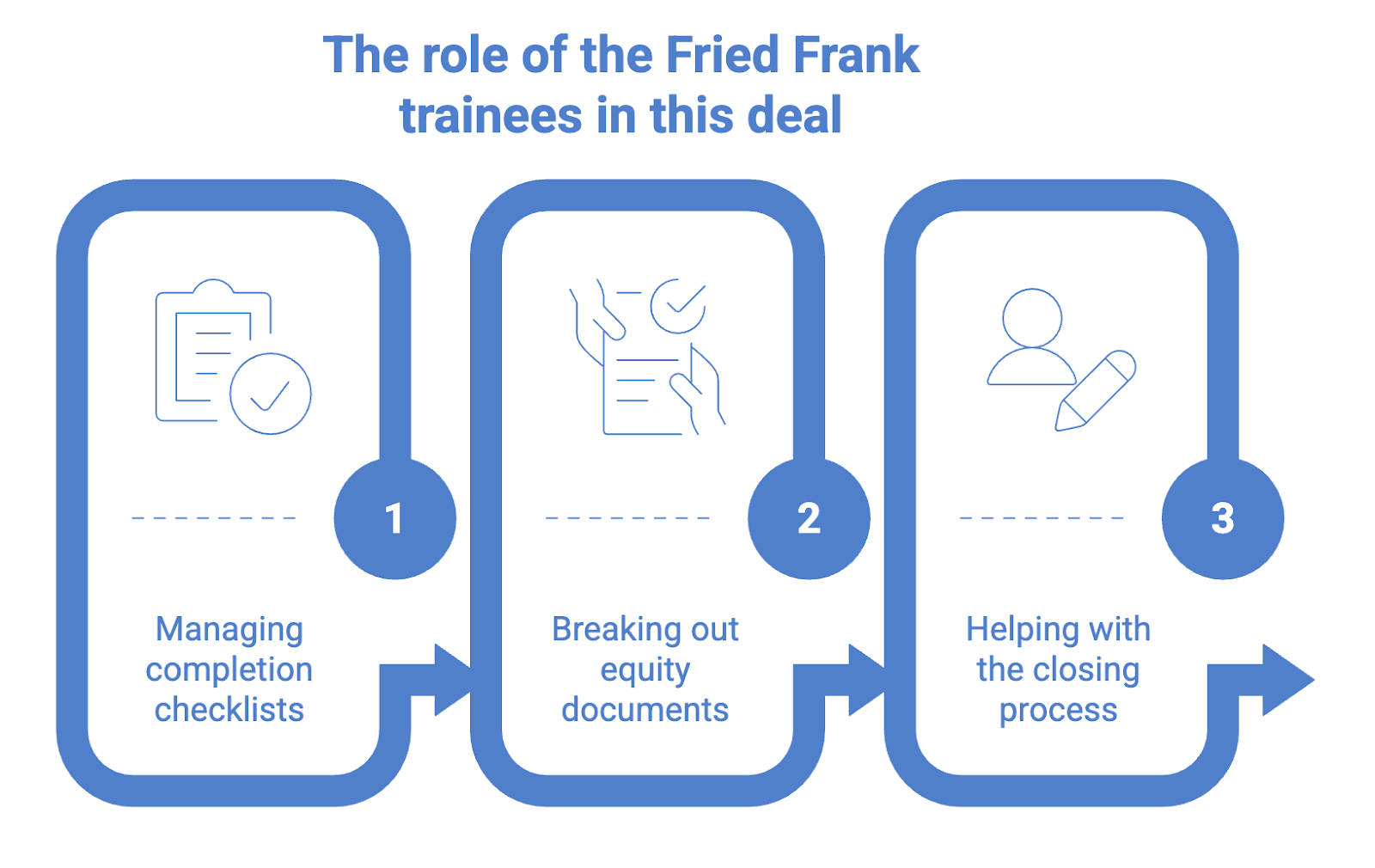

What did Fried Frank’s trainees actually do?

Trainees and junior lawyers were involved throughout the deal. Their work was essential to keeping the transaction moving.

🖊️ Signing and completion checklists: Trainees and junior associates were involved in updating signing and completion checklists. This involved spotting anything that was outstanding early on and flagging it to the senior members of the team. This work trained the juniors to remain organised, assume responsibility for certain deliverables and communicate clearly with the wider team.

📄 Breaking out equity documents: Once template forms were agreed for the documents, trainees and junior associates took the subscription forms and other equity documents and tailored them for each manager – inserting the right share numbers and subscription amounts. This needed attention to detail to produce signing-ready versions of the documents.

🤝 Assisting with closing mechanics: In the run-up to closing, juniors helped analyse and finalise the funds flow (a spreadsheet that shows who gets paid what on completion). This involved checking the purchase price, the debt repayment amounts, and the fees payable to banks, lawyers and other advisers. They made sure the numbers were correct and matched the transaction documents. It also gave juniors exposure to the TowerBrook deal team and the financial advisers working on the transaction.

At Fried Frank, trainees are actually involved in transactions like this. They manage checklists, finalise key documents, review funds flows, manage the completion process and help keep deals moving day to day.

Are you interested in applying to Fried Frank?

Did this newsletter help you learn more about the private equity work Fried Frank does?Please share a reason after you vote (it really helps us) |

Your responses are a huge help in us getting to do more with law firms.

AROUND THE WEB 🌐

🔤 Word play: This Nonsense Lab (from Google) lets you twist and manipulate the way words are spelled and sound

🚉 Commute: Enter how long your commute is and this site builds an exact Wikipedia rabbit hole that fits exactly into the time you have

🎵 Discover: Put in three artists you love and this tool gives you a personalised list of new music to explore

STUFF THAT MIGHT HELP YOU 👌

💻️ Free application advice: Check out my YouTube channel for actionable tips and an insight into the lifestyle of a commercial lawyer in London.

📁 Law firm application bank: A growing library of real, verified successful applications for training contracts and vacation schemes. Helpful if you want to learn from others who answered the same questions you’re stuck on.

📝 Write winning law firm applications: A practical course to help you write clearer applications, faster. Avoid common mistakes, learn how to structure answers properly, and get lifetime access to future updates. Try it for 14 days, risk free.

How did you find today's newsletter? |