- LittleLaw

- Posts

- 🍦 How Linklaters carved out an €8 billion ice cream empire

🍦 How Linklaters carved out an €8 billion ice cream empire

Idin Sabahipour

April 15, 2026

Together with

Table of Contents

If you take just one thing from this email...

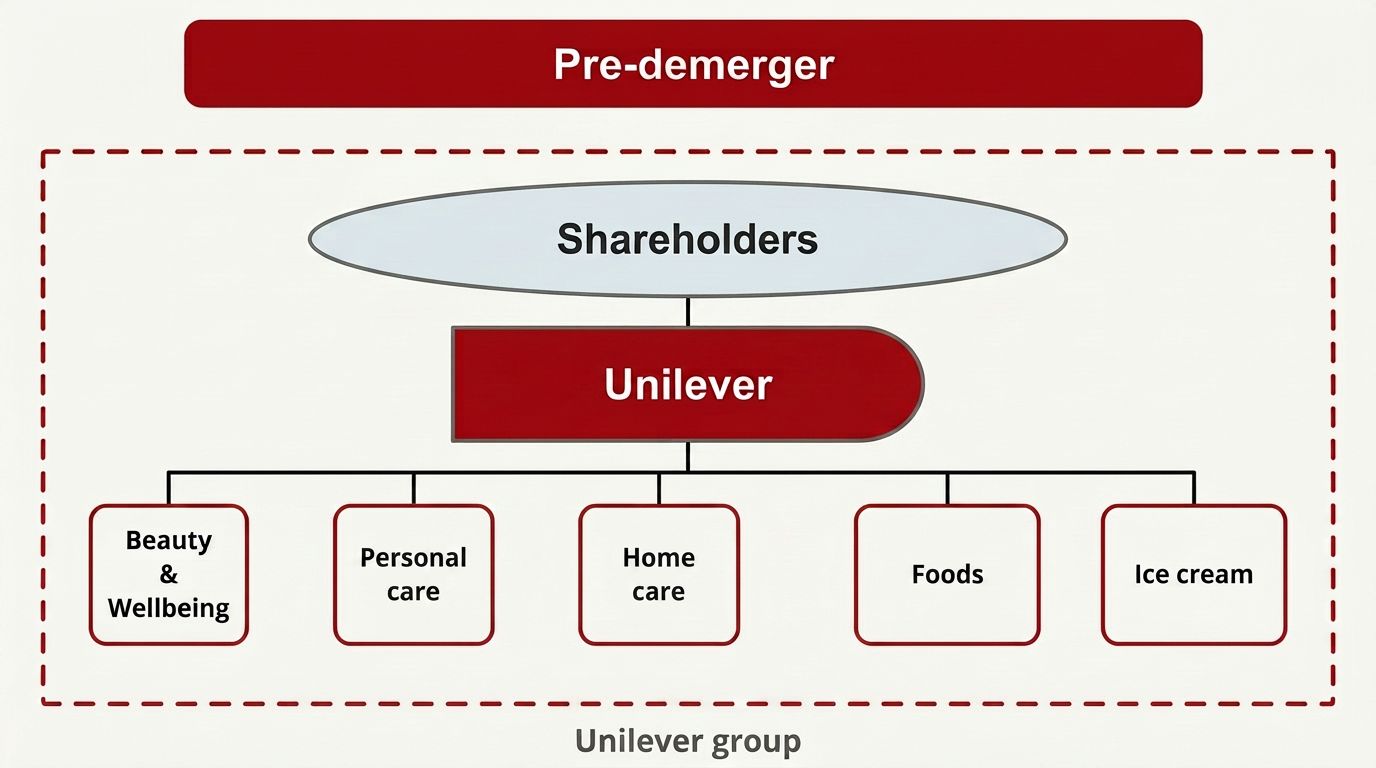

Unilever wanted to get rid of its ice cream business – but instead of selling it, it chose a "demerger." That meant spinning it off into a brand new company and giving existing Unilever shareholders shares in that new company. The key differences from a sale are that no money changes hands and shareholders still benefit from future growth.

EDITOR’S RAMBLE 🗣

It's vac scheme season.

So, I put together a guide with everything I wish I'd known before my first vac scheme.

One tip that helped me – send your supervisor a weekly summary of everything you've worked on. It’s not to try and show off. It’s because your supervisor’s going to be asked about their thoughts on your work. And (if you don’t tell them) they won’t know everything you did.

Send a quick table on a Friday afternoon, and you make their job much easier when it comes to writing your feedback (which helps you get your TC).

There are 9 other uncommon tips in the guide.

I’m super excited about this week's newsletter – the Linklaters deal that separated Unilever's ice cream business across 80+ countries.

It's one of the biggest pieces of legal work we've ever covered. And the Linklaters team walked us through exactly what happened.

Once you've read it, complete the poll (at the bottom) to let me know your thoughts.

– Idin

FEATURED REPORT 📰

🍦 How Linklaters carved out an €8 billion ice cream empire

What’s going on here?

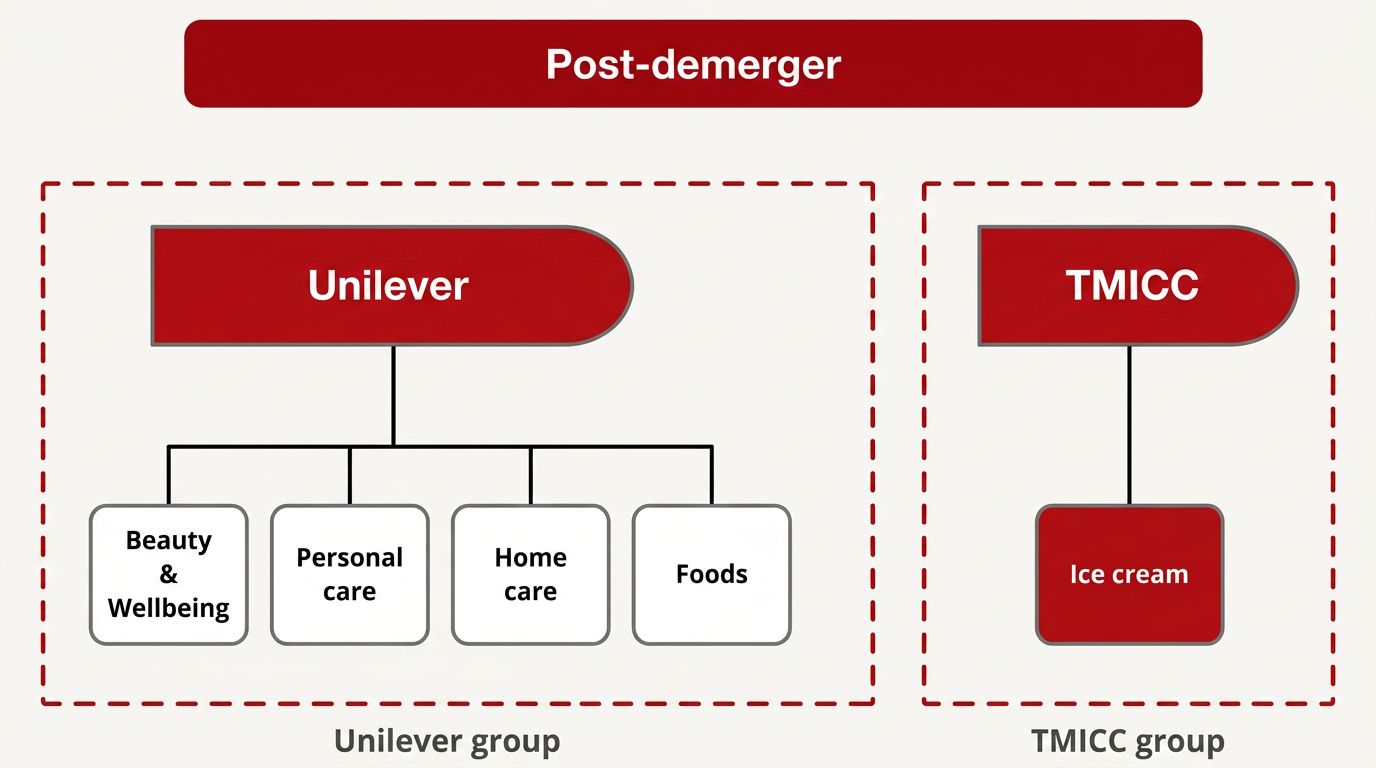

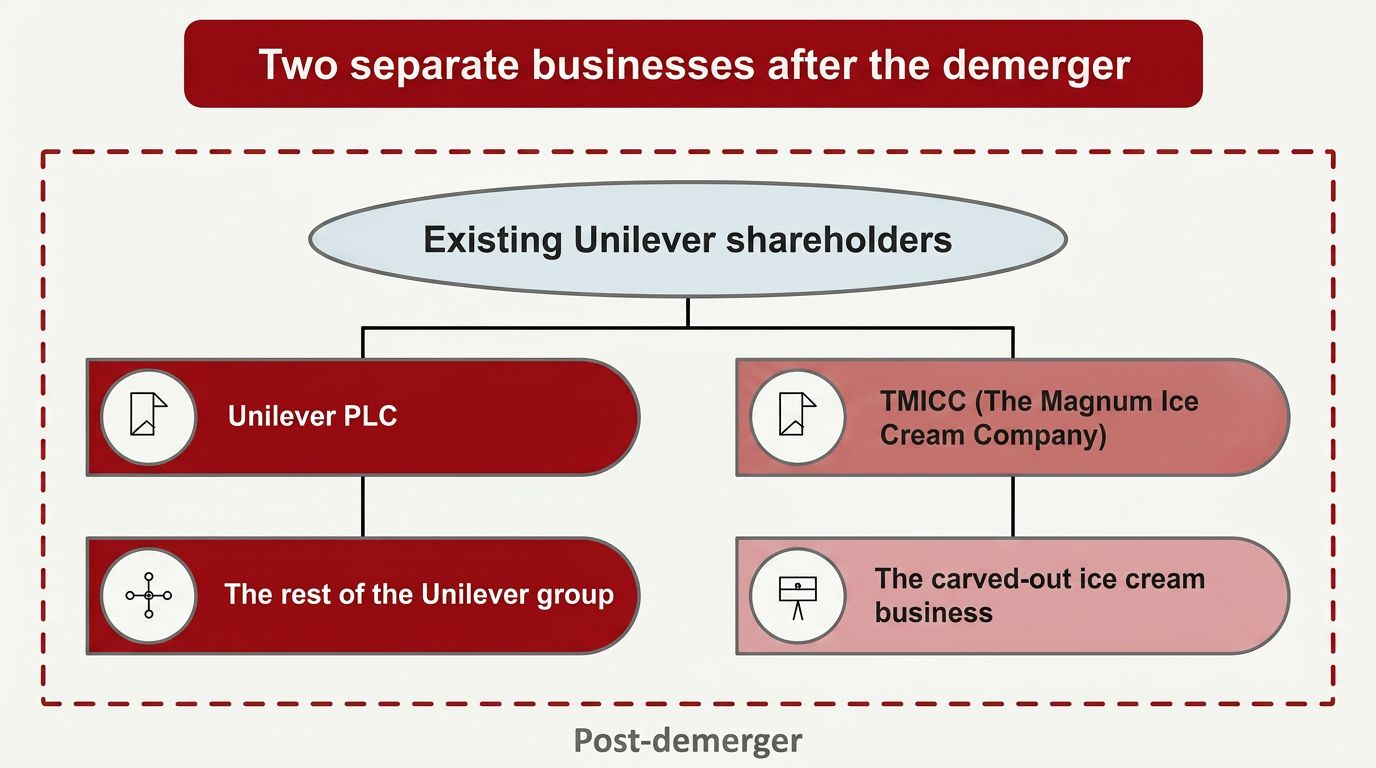

Unilever is one of the world's largest consumer goods companies – it’s behind brands like Dove, Hellmann's and Persil. In December last year, it separated its entire ice cream division (including Magnum, Ben & Jerry's, Wall's, and Cornetto) into a brand-new standalone company called The Magnum Ice Cream Company (or “TMICC”).

Linklaters led the legal work on this. They helped separate the ice cream business from Unilever across more than 80 countries, and also managed a triple listing process.

Why did Unilever want to separate its ice cream business?

Ice cream is a fundamentally different business to the rest of Unilever's portfolio.

🌡️ Seasonal demand: Most of Unilever's products – Dove soap, Hellmann's mayonnaise, Persil – sell steadily year-round. But with ice cream, demand spikes in summer and dips in winter, which makes revenue less consistent than the rest of the portfolio.

🚛 Cold chain logistics: Ice cream needs specialist refrigerated storage and transport from factory to shop freezer. That's an entirely separate (and more expensive) supply chain to Unilever's other products.

📈 A case for independence: Unilever's view was that its ice cream business could grow faster as a standalone company, with its own leadership team, its own strategy and the freedom to raise funding on its own terms. At the same time, separating it would let Unilever focus on its faster-growing segments.

Why didn't Unilever just sell the ice cream business?

When a company wants to offload a division, the most common route is a sale – find a buyer, agree a price, transfer it over. But if Unilever did that, it would mean its shareholders lose the benefit of future growth in the ice cream business.

Instead, Unilever chose a “demerger”.

🤔 What is a demerger?

A demerger is when a company separates part of its business into a new, independent company. Instead of selling it, the parent company distributes shares in the new company to its existing shareholders – so they end up holding shares in both (no cash changes hands).

So if you owned Unilever shares before the split, you automatically received TMICC shares too – no need to buy them separately.

But here's where it gets more technically challenging. The legal structure had to work across three different public markets. Unilever is listed in Amsterdam, London and New York, and its shareholders hold their shares through different systems depending on where they're based (each stock exchange has its own settlement system for recording who owns what). The demerger had to deliver TMICC shares to every shareholder in the same place they already held their Unilever shares so nobody had to go looking for them in a different system.

How do you actually separate a business that operates in 80+ countries?

Unilever is a huge corporation, operating in 190+ countries – and its ice cream business wasn't a neat, self-contained part of Unilever. It was fully integrated into Unilever's wider operations – sharing IT systems, logistics networks and back-office functions.

That meant it wasn't possible to completely separate the two businesses before the demerger. So Unilever entered into a number of services arrangements (including transitional services agreements) with TMICC. Under those arrangements, Unilever would continue providing certain services for a set period after the split – this could be things like payroll, data storage, and order management systems – while TMICC built its own operations.

🤔 What is a transitional services agreement?

A TSA is a contract where the former parent company agrees to keep providing certain services to the newly separated business for a set period after the split. Think of it like moving out of a shared flat but sharing your old housemate's Netflix login for a while until you set up your own.

Designing those transitional arrangements across 80+ countries was one of the biggest pieces of legal work on this deal. Each jurisdiction had its own challenges. Some countries had local manufacturing operations, others were distribution-only – and each came with different rules around outsourcing, employment and tax.

On top of that, TMICC now needed its own licences and permits in every country – to manufacture food, employ staff and operate independently (it couldn't rely on Unilever's anymore). Every new company had to be formally set up, and every licence had to be in place, before TMICC could stand on its own.

But the operational separation was only half the picture – TMICC also had to list as a public company, simultaneously, on three stock exchanges.

What's involved in listing a new company on three stock exchanges at the same time?

Once the business was separated, TMICC then needed to list as a public company – which meant publishing a prospectus (a legal document that’s required before a company’s shares can be traded). A prospectus tells potential investors everything they need to know – the business, its finances and the risks involved – so they can make an informed decision about whether to invest.

Because TMICC was listing in Amsterdam, London and New York, that prospectus needed approval from three regulators at the same time:

🇳🇱 the AFM in the Netherlands,

🇬🇧 the FCA in the UK, and

🇺🇸 the SEC in the US.

🤔 Can one company be listed on multiple stock exchanges?

Yes – it's called a dual listing (or in this case, a triple listing).

A company's shares are traded on more than one exchange at the same time, which gives investors in different countries easier access to buy and sell those shares.

It's not uncommon for large multinational corporations – Unilever itself is listed in Amsterdam, London and New York, and TMICC now trades on all three exchanges too.

🔍 Different regulators, different focus areas: Even though the UK and EU Prospectus Regulation were largely the same on paper, the AFM and FCA sometimes focus on different things in their reviews. Navigating those competing comments on a single document, without creating inconsistencies, needs the lawyers to coordinate their responses well.

⚠️ The “Risk Factors” section: Every prospectus includes a section called Risk Factors, which is closely scrutinised by regulators. This is where the company sets out the most serious risks that could affect its business or its share price – so that investors know what they're getting into before they decide to invest. For example, TMICC might need to flag that its revenue is seasonal (with lower sales in the winter).

Since it’s related to the day-to-day running of the business, this section is drafted by lawyers working closely with the company. Plus, it has to be updated throughout the entire process. If new risks emerge along the way – say, a new food safety regulation that will materially affect the company’s business in a key market – they need to be reflected before publication.

🏛️ The SEC shutdown: Then came an unexpected delay. In October 2025, the US federal government entered a shutdown – and the SEC stopped reviewing the prospectus entirely.

The demerger was originally set to complete on 10 November, but had to be pushed back. Linklaters had to find a different regulatory path to get the prospectus published in New York while the AFM and FCA continued on their own timetable.

The deal finally completed on 6 December 2025.

What did junior lawyers actually do on this deal?

Trainees and junior associates were heavily involved – particularly on the operational separation work. The scale of this deal meant there were real opportunities for trainee involvement.

🌍 Owning entire countries: The Linklaters team allocated individual countries to trainees and junior associates. Each junior was involved in all elements of the separation in their assigned countries – from getting new companies formally set up and registered, to coordinating with local counsel, to gathering the required information from Unilever's legal team on the ground. Instead of having one narrow task on a huge deal, each junior had a full picture of how the separation played out in their countries.

🤝 Working with local counsel: For each country, Linklaters worked with local law firms who knew the domestic rules. The juniors were often the main point of contact – reaching out to local counsel, getting advice on what was needed to register a new entity or transfer a business, and then working with the client to progress that process. They also provided regular status updates to the wider team, maintained trackers and flagged issues as they came up.

⭐️ Why this matters: On a deal that involved 80+ jurisdictions, this kind of work isn't peripheral – it's actually what keeps the whole thing moving. The Linklaters trainees were encouraged to take ownership, and build working relationships with both local counsel and Unilever contacts directly. That's the kind of client-facing, cross-border exposure that not all law firms offer this early in your career.

What bigger picture trends does this deal show?

This deal reflects a few broader shifts that aspiring commercial lawyers should be aware of.

🏢 The age of the conglomerate is fading. Large multinationals like Unilever are increasingly deciding that owning lots of different businesses under one roof isn't the best way to create value. Recently, GE (an American industrial conglomerate) split into three focused companies, and Johnson & Johnson spun off Kenvue, its consumer health business. Investors want focus – and companies are listening. Unilever has already sold its tea business and its spreads division in recent years (Linklaters advised on both). Expect more of these complex portfolio separations from major corporations.

🌍 Cross-border demergers are becoming more common (and more complex). A demerger across 80+ countries, with triple listings and three simultaneous regulatory processes, is a huge legal exercise. Since businesses have become more globally integrated, unwinding them is a bigger job. That means more work for firms with genuine global reach – and more demand for lawyers who have experience with multi-jurisdictional work of this scale.

⚖️ These deals take lawyers beyond the legal work. For the Linklaters team, the most interesting element of this deal was the exposure to non-legal parts of the client's business – supply chain, marketing, real estate, HR. On a full carve-out, lawyers need to deeply understand how the business actually operates in order to separate it properly. It's legal work, but it's deeply rooted in the commercial reality of the business.

You might have written “I want to work on complex, cross-border transactions” in an application before.

Now you know exactly what that looks like in practice (and in your next Linklaters application) you've got a strong deal to show for it.

IN OTHER NEWS 🗞

⚖️ The biggest change to UK employment law in a generation has just taken effect. Key parts of the Employment Rights Act 2025 came into force last week, giving workers day-one rights to paternity and parental leave and scrapping the waiting period for statutory sick pay. This puts more pressure on businesses, and there’s a new Fair Work Agency that has launched to enforce the rules. Here’s a useful guide from Pinsent Masons.

🍽️ The Ivy, Annabel's and Scott's have all been sold. British businessman Richard Caring has sold a majority stake in his portfolio of iconic London venues (including Sexy Fish and Harry's Bar) to Abu Dhabi-backed investor DIAFA in a deal worth £1.4 billion. Caring will stay on as executive chairman, and there are already plans to expand The Ivy into the US. HSF Kramer advised Caring, and Norton Rose Fulbright acted for DIAFA.

📝 Four out of five SQE candidates say the exam is not fit for purpose. A survey by the National Junior Lawyers Division found that 82% also think it's poor value for money – with nearly half of respondents spending over £10,000 on preparation and fees. The NJLD is now calling for a review of exam costs, better feedback on failed assessments, and tighter regulation of course providers.

AROUND THE WEB 🌐

🪟 Views: Look out of real people's windows from around the world

🏛️ Up close: Explore thousands of artworks from New York’s Met Museum in 3D – rotate, zoom, and examine everything

🥑 Tasty: Mexico smashed the Guinness record with 6,800 kilos of guacamole

STUFF THAT MIGHT HELP YOU 👌

💻️ Free application advice: Check out my YouTube channel for actionable tips and an insight into the lifestyle of a commercial lawyer in London.

📁 Law firm application bank: A growing library of real, verified successful applications for training contracts and vacation schemes. Helpful if you want to learn from others who answered the same questions you’re stuck on.

📝 Write winning law firm applications: A practical course to help you write clearer applications, faster. Avoid common mistakes, learn how to structure answers properly, and get lifetime access to future updates. Try it for 14 days, risk free.

How did you find today's newsletter? |